Fund Commentaries

3Q 2023 Commentary

3rd Quarter 2023

Summary

- Performance

- Country & Oil&Gas Thoughts

- Key Movements & Weightings

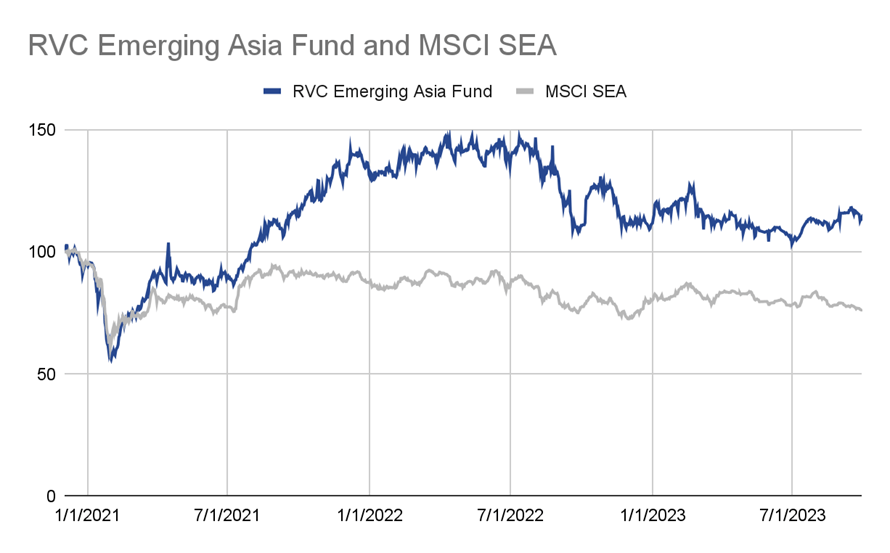

Performance

Over the past three years, the RVC Emerging Asia Fund returned +30.8%, versus the MSCI ASEAN which returned +1.6%.

In the Third Quarter of 2023, the RVC Emerging Asia Fund returned +9.3% versus the MSCI ASEAN which decreased -2.4%.

Year to date, the RVC Emerging Asia Fund returned -2.5% versus the MSCI ASEAN which decreased -6.4%.

Country Thoughts & Weighting

Oil & Gas

As the world continues to be a volatile environment there is one sector that is increasing capex, something unheard of in the past decade. The Oil & gas sector. Our holdings in this sector is one of the key reasons to continue outperforming the region over the past three years, more recently with MEDC IJ increasing +70% during the third quarter alone.

While media headlines and government policies have tirelessly championed renewable energy and sustainability, the stark reality remains that the global economy and its consumers continue to rely on fossil fuels. The past decade bore witness to a conspicuous disappearance of oil and gas capex, brought about by the tandem forces of depressed oil prices and the onerous ESG restrictions self-imposed by financial institutions, restraining their lending for oil and gas projects.

Consequently, this prolonged drought of projects resulted in the stark consolidation of the oil and gas service provider landscape. Startlingly, an estimated 80% of key players in the sector within the region either succumbed to bankruptcy or were absorbed into new entities since 2014, creating a supply constraint.

However, the landscape is shifting as higher oil prices in recent years have breathed fresh life into the industry. Notably, Shell's recent announcement of pivoting away from renewable ventures to refocus on its core cash-generating business has set the stage for exploration and production (E&P) majors to embark on new projects. This shift is regionally palpable, with PTT Group in Thailand announcing capital expenditures for the Gulf of Thailand, Petronas in Malaysia unveiling ambitious plans, increasing its capital expenditures significantly for 2023 - 2025, and PetroVietnam expanding its footprint in Vietnam with Block B. These endeavours represent multi-year undertakings that signal a resurgence in the sector.

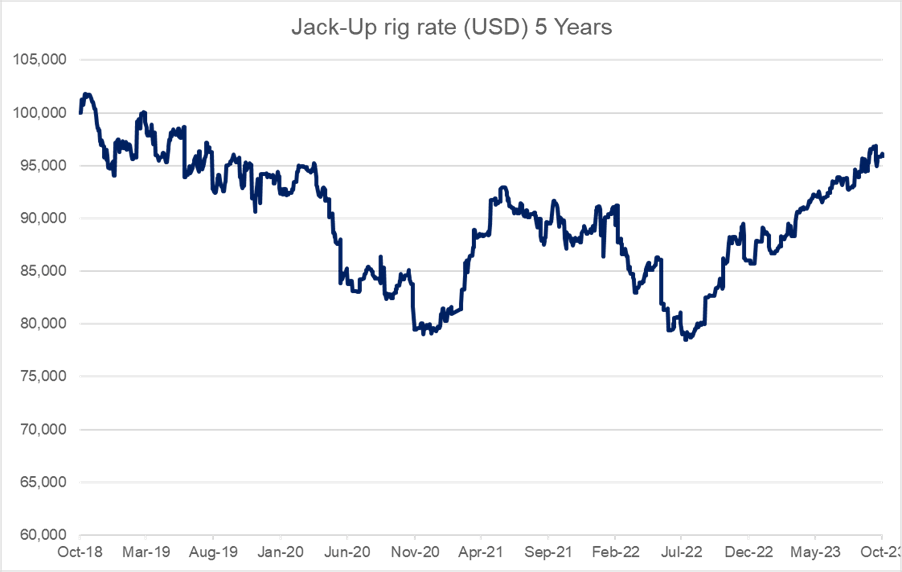

In this new scenario, characterised by a scarcity of service suppliers, there's a scramble to secure contracts and services by the E&P giants. This heightened demand is met with a bottleneck in supply, affording the service providers the upper hand in setting prices, a favourable position they've not enjoyed in quite some time.

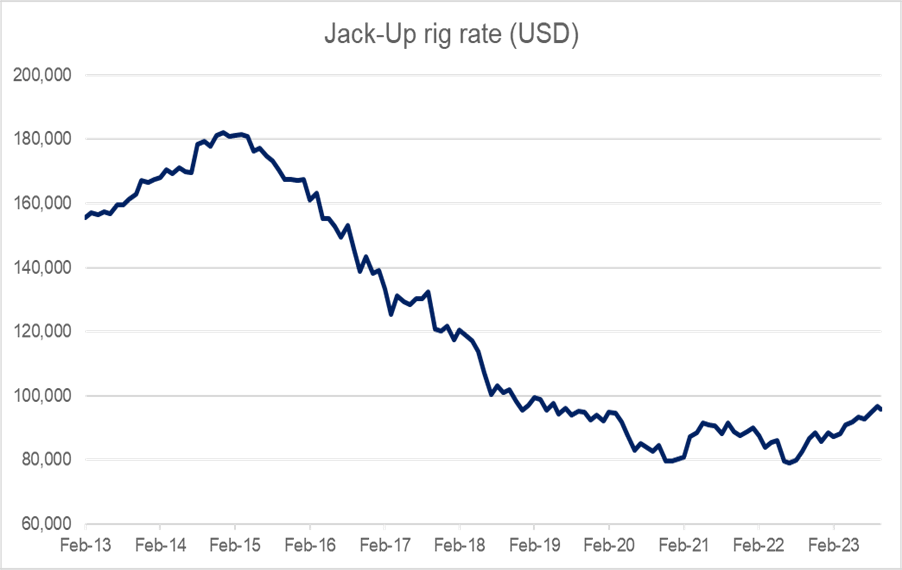

An example of this is the daily jack-up rig rates, since the low point in 2022, the daily Jack-Up rig rates have increased by +25%.

However over the past decade, the daily rates are still -50% from their previous peak.

Over the past few months and in the upcoming weeks, our fund is poised to incrementally strengthen its positions in several key players within the region. This industry is exceptionally well-positioned to prosper well into 2024 and onwards. As a testament to our confidence, our fund already commands a 5% stake in VEB MK, a company we've previously elaborated upon. Further reinforcing our commitment, you will find below a discussion of our new 4% stake in CSE SP. By year-end, the fund's allocation into this sector is slated to reach close to 20%, underlining our conviction in the oil and gas sector's resurgence as a formidable force in the global energy landscape.

Vietnam

Last quarter we wrote that “We are positive on Vietnam’s stock market potential performance, however we are not overtly positive about the economic outlook for Vietnam.” Since then the country’s stock market has performed very well and we have subsequently reduced the weighting by half from 30% to 17% during the Third Quarter of 2023 and within the first weeks of the Fourth Quarter reduced it to 10%. Why? First and foremost, the government's earnest efforts to curb corruption have inadvertently wounded the very feet they stand upon. While a commendable drive, the zeal with which this anti-corruption campaign was executed sent shockwaves through the business landscape, stifling investor confidence and triggering a wave of uncertainty. Adding to the turmoil is the real estate crisis that has left the nation grappling with an increasing amount of NPLs, a lack of new development and thus plummeting credit growth from the financial institutions. With real estate having played a pivotal role in the Vietnamese economic landscape, this crisis has cast a long shadow on the nation's fiscal health. Further compounding Vietnam's economic predicament is a slowdown in manufacturing orders from Western nations. This deceleration can be traced back to a phenomenon known as 'overordering' in 2021 and 2022, resulting in bloated inventories that now haunt the manufacturing sector. Yet, it is the energy conundrum in Northern Vietnam that casts the most ominous pall. With a staggering 43% of their energy supply hinging on hydroelectric power, the nation is rendered vulnerable during low-water periods, leaving many residents literally in the dark. This energy fragility underscores the need for diversification and long-term energy infrastructure planning. Nonetheless, it would be imprudent to dismiss Vietnam's innate economic strengths. A business-focused culture, promising demographics, and a steady influx of Foreign Direct Investment (FDI) continue to paint a favourable long-term narrative for the nation. Despite the storm clouds, the silver lining of potential remains discernible. And should attractive valuations reappear in the future we would accordingly increase our positions in Vietnam.

Key Movements & Weightings

Key Movements

The key movements during the quarter were as follows:

Exits

BCP TB (Mkt cap: THB 58 bn/USD 1.6 bn)

Bangchak Plc (BCP TB) was one of the oil & gas related positions that we initiated during 1Q23, as the share price rallied ~20% as the market began pricing in the ESSO acquisition as well as the increase in GRM’s we fully exited the position.

MAPA IJ (Mkt Cap: IDR 22.5 trn/USD 1.4 bn)

Map Aktif Adiperkasa PT (MAPA IJ) was a covid-era position (2021) that focused on the recovery post reopening. It is the leading lifestyle retailer/distributor/franchisee in SE Asia with over 2,300 retail stores and a diversified portfolio of over 150 brands that includes sports, fashion, department stores, kids, food & beverage and lifestyle products. Some iconic brands include Starbucks, Zara, Marks & Spencer, SOGO, Galeries Lafayette, LEGO, Apple, Hasbro, adidas among many others. The company’s operating performance surpassed our expectations in 2023 and this contributed to the share price rallying nearly 3x since 2021, we fully exited the position during 3Q23.

VPB VN (Mkt Cap: VND 150 trn/USD 6.1 bn)

VPB is one of the best performing private financial institutions in Vietnam, during the 3rd Quarter of 2023, the long awaited investment deal of Sumitomo Mitsui Banking Corporation taking a 15% stake was completed. As a function of the share price rallying strongly since we acquired additional shares during 2H23 we fully exited the position.

Existing holdings

GMD VN (Mkt Cap: VND 19.8 trn/USD 804 mn)

Gemadept, the preeminent port operator in Vietnam. Our steadfast confidence in Gemadept stems from its role as the premier conduit for harnessing the influx of Foreign Direct Investment (FDI) into Vietnam. A recent on-site assessment reaffirms our conviction, even in the face of a global economic slowdown. Gemadept remains adept at steadily expanding its market share, bolstered by robust export volume growth and the promising potential of forging equity partnerships with major shipping corporations. Additionally, the imminent prospect of raising fee tariffs and deep-water port terminal handling charges adds another layer of investment appeal.

Vietnam Maritime Administration's ongoing efforts to craft a circular aimed at revamping regulated port fees hold strategic significance. This initiative, albeit delayed due to pandemic-induced disruptions, is pivotal for players like Gemadept. The agreements previously inked allowed for incremental fee hikes of up to 10% every three years, but were hindered by COVID-related delays. In terms of international cargo, the draft circular introduces a noteworthy increase in the floor price for non-deep-water ports, alongside a lift in the ceiling price for various ancillary fees like berth and marine pilot charges. Furthermore, the deep-water port terminal handling charges (THC) are slated for a 10% boost.

Of particular interest is the prospective 21% THC increase at the deep-water Gemalink port, should the circular gain approval. Gemalink, which currently quotes THC at the prevailing ceiling rate, would witness a consequent approximate 13% ascent in its Average Selling Price (ASP). However, for non-deep-water ports under Gemadept's purview, including Nam Hai, Nam Dinh Vu, Phuoc Long, and Binh Duong ICD, the impact of the increased floor price in the new circular is expected to be minimal, given that their THC rates already surpass the stipulated floor price.

In conclusion, Gemadept's strategic positioning in the Vietnamese port sector, combined with its potential for revenue expansion through fee increases and burgeoning partnerships, makes it an attractive proposition within our portfolio. The evolving landscape of regulated port fees further amplifies its investment allure, presenting us with a well-positioned opportunity to navigate the intricacies of this dynamic market.

New holdings

CSE SP (Mkt Cap: SGD 255.2 mn/USD 185.8 mn)

CSE Global, a dynamic systems integrator, is a compelling player in the provision and installation of process control systems, turnkey telecommunication solutions, and security solutions, with a pronounced focus on the energy, infrastructure, and mining & minerals sectors. Notably, its expertise lies in SCADA, DCS, PLCs, and plant systems, primarily servicing the oil, gas, and power facilities. Recently securing two significant contracts, the company is poised for substantial growth. One contract involves designing, manufacturing, and integrating power distribution centres and electrical systems in the US from 2023 to 2025, while the other pertains to communication and security systems for the Singapore government.

As of the end of 1H23, CSE Global's order book stood at SGD 520 million, and it is on track to reach SGD 900 million by year-end. The company's financial outlook is impressive, with profit growth projections as follows: +300% for the current year, +30% in 2024, and +25% in 2025. This translates to attractive valuations, with a price-to-earnings (PE) ratio of 10x for 2024 and 7x for 2025. Furthermore, investors can anticipate robust dividend yields of 6% and 8% for 2024 and 2025, respectively.

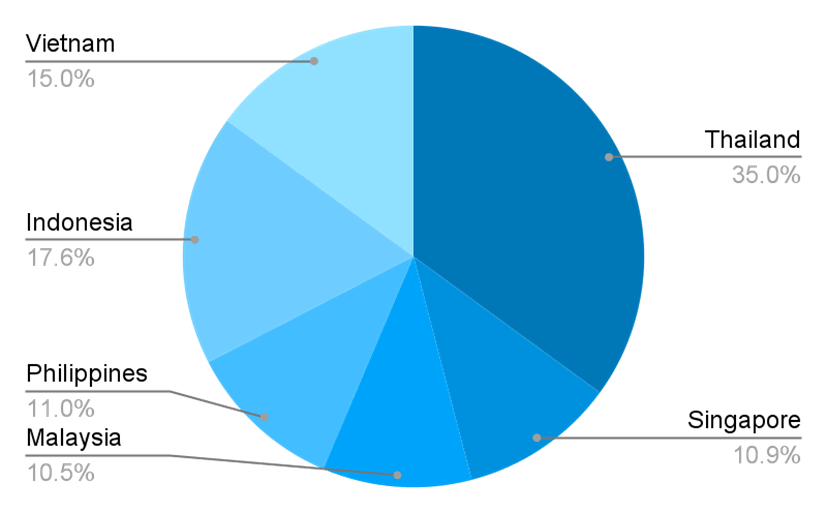

Weightings by Category

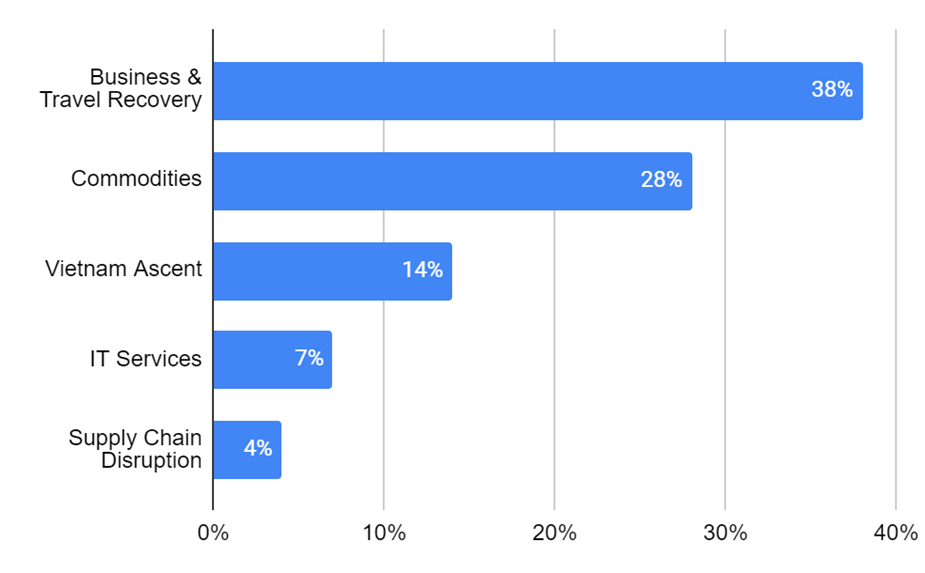

Top 5 Sector Weightings

Top 5 Positions (accounting for 29% of the Fund)

- MEDC IJ

- WPH TB

- MWG VN

- VEB MK

- CSE SP

Top Contributors during 3Q23

Positive: MEDC IJ, DGW VN, HIBI MK, WPH TB, GMD VN

Negative: SHR TB, BVG TB, SIDO IJ, DNL PM, MAC PM

Currency

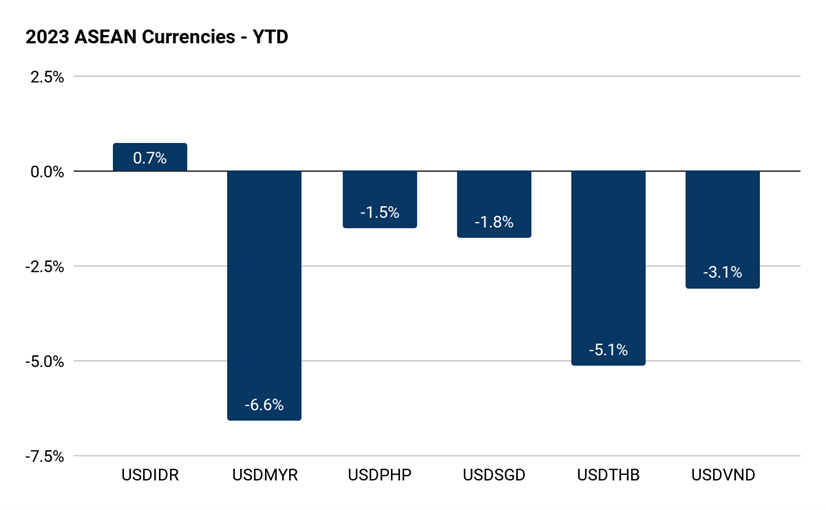

As of the end of September 2023, the strongest performing currency is the Indonesian Rupiah, the weakest performing currencies are the Malaysian Ringgit and the Thai Baht.

Tickers mentioned

- BCP TB - BANGCHAK CORP PCL

- CSE SP - CSE GLOBAL LTD

- DNL PM - D&L INDUSTRIES

- DGW VN - DIGIWORLD

- GMD VN - GEMADEPT CORP

- HIBI MK - HIBISCUS PETROLEUM BHD

- MAC PM - MACROASIA CORPORATION

- MAPA IJ - MAP AKTIF ADIPERKASA PT

- MEDC IJ - MEDCO ENERGI INTERNASIONAL T

- SHR TB - S HOTEL & RESORTS

- SIDO IJ - SIDO MUNCUL

- VEB MK - VELESTO ENERGY

- VPB VN - VIETNAM PROSPERITY JSC BANK

- WPH TB - WATTANAPAT HOSPITAL